Chapter 11 Assignment 1: Basic Programming in R

Report the following results in html format using R markdown. In other words, replicate this document. You write functions in a separate R file and put in R folder in the project folder. Build the project as a package and load it from the R markdown file. The execution code sholuld be written in R markdown file.

You submit:

- R file containing functions.

- R markdown file containing your answers and executing codes.

- HTML(or PDF) report generated from the R markdown.

11.1 Simulate data

Consider to simulate data from the following model and estimate the parameters from the simulated data.

\[ y_{ij} = 1\{j = \text{argmax}_{k = 1, 2} \beta x_k + \epsilon_{ik} \}, \] where \(\epsilon_{ik}\) follows i.i.d. type-I extreme value distribution, \(\beta = 0.2\), \(x_1 = 0\) and \(x_2 = 1\).

- To simulate data, first make a data frame as follows:

## # A tibble: 2,000 × 3

## i k x

## <int> <int> <dbl>

## 1 1 1 0

## 2 1 2 1

## 3 2 1 0

## 4 2 2 1

## 5 3 1 0

## 6 3 2 1

## 7 4 1 0

## 8 4 2 1

## 9 5 1 0

## 10 5 2 1

## # ℹ 1,990 more rows- Second, draw type-I extreme value random variables. Set the seed at 1. You can use

evdpackage to draw the variables. You should get exactly the same realization if the seed is correctly set.

## # A tibble: 2,000 × 4

## i k x e

## <int> <int> <dbl> <dbl>

## 1 1 1 0 0.281

## 2 1 2 1 -0.167

## 3 2 1 0 1.93

## 4 2 2 1 1.97

## 5 3 1 0 0.830

## 6 3 2 1 -1.06

## 7 4 1 0 -0.207

## 8 4 2 1 0.617

## 9 5 1 0 0.0444

## 10 5 2 1 1.92

## # ℹ 1,990 more rows- Third, compute the latent value of each option to obtain the following data frame:

## # A tibble: 2,000 × 5

## i k x e latent

## <int> <int> <dbl> <dbl> <dbl>

## 1 1 1 0 0.281 0.281

## 2 1 2 1 -0.167 0.0331

## 3 2 1 0 1.93 1.93

## 4 2 2 1 1.97 2.17

## 5 3 1 0 0.830 0.830

## 6 3 2 1 -1.06 -0.863

## 7 4 1 0 -0.207 -0.207

## 8 4 2 1 0.617 0.817

## 9 5 1 0 0.0444 0.0444

## 10 5 2 1 1.92 2.12

## # ℹ 1,990 more rows- Finally, compute \(y\) by comparing the latent values of \(k = 1, 2\) for each \(i\) to obtain the following result:

## # A tibble: 2,000 × 6

## i k x e latent y

## <int> <int> <dbl> <dbl> <dbl> <dbl>

## 1 1 1 0 0.281 0.281 1

## 2 1 2 1 -0.167 0.0331 0

## 3 2 1 0 1.93 1.93 0

## 4 2 2 1 1.97 2.17 1

## 5 3 1 0 0.830 0.830 1

## 6 3 2 1 -1.06 -0.863 0

## 7 4 1 0 -0.207 -0.207 0

## 8 4 2 1 0.617 0.817 1

## 9 5 1 0 0.0444 0.0444 0

## 10 5 2 1 1.92 2.12 1

## # ℹ 1,990 more rows11.2 Estimate the parameter

Now you generated simulated data. Suppose you observe \(x_k\) and \(y_{ik}\) for each \(i\) and \(k\) and estimate \(\beta\) by a maximum likelihood estimator. The likelihood for \(i\) to choose \(k\) (\(y_{ik} = 1\)) can be shown to be: \[ p_{ik}(\beta) = \frac{\exp(\beta x_k)}{\exp(\beta x_1) + \exp(\beta x_2)}. \]

Then, the likelihood of observing \(\{y_{ik}\}_{i, k}\) is: \[ L(\beta) = \prod_{i = 1}^{1000} p_{i1}(\beta)^{y_{i1}} [1 - p_{i1}(\beta)]^{1 - y_{i1}}, \] and the log likelihood is: \[ l(\beta) = \sum_{i = 1}^{1000}\{y_{i1}\log p_{i1}(\beta) + (1 - y_{i1})\log [1 - p_{i1}(\beta)\}. \]

- Write a function to compute the likelihood for a given \(\beta\) and data and name the function

compute_loglikelihood_a1(b, df).

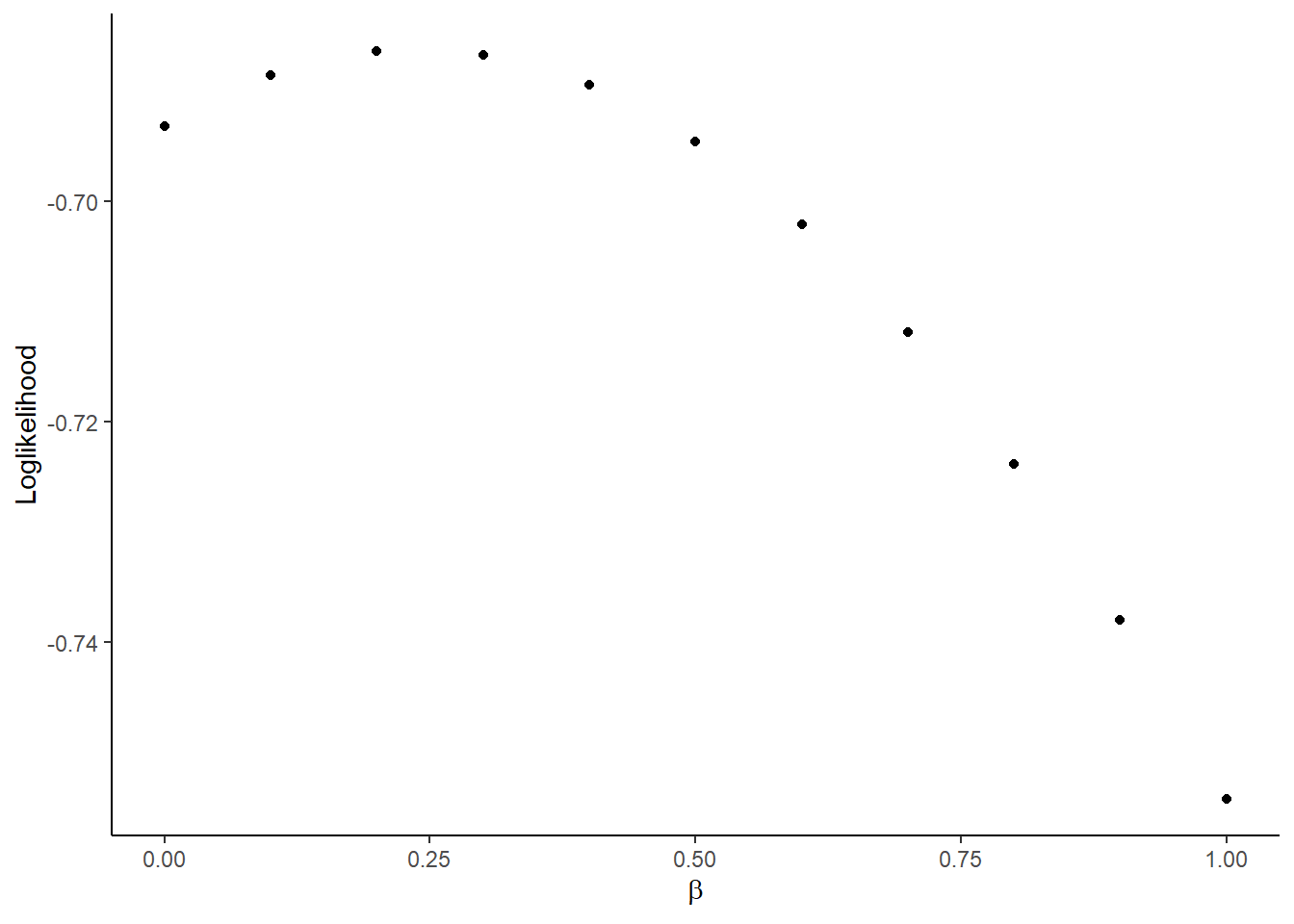

## [1] -0.7542617- Compute the value of log likelihood for \(\beta = 0, 0.1, \cdots, 1\) and plot the result using

ggplot2packages. You can uselatex2exppackage to use LaTeX math symbol in the label:

b_seq <- seq(0, 1, 0.1)

output <-

foreach (

b = b_seq,

.combine = "rbind"

) %do% {

l <-

compute_loglikelihood_a1(

b,

df

)

return(l)

}

output <-

data.frame(

x = b_seq,

y = output

)

output %>%

ggplot(

aes(

x = x,

y = y

)

) +

geom_point() +

xlab(TeX("$\\beta$")) +

ylab("Loglikelihood") +

theme_classic()

- Find and report \(\beta\) that maximizes the log likelihood for the simulated data. You can use

optimfunction to achieve this. You will useBrentmethod and set the lower bound at -1 and upper bound at 1 for the parameter search.

## $par

## [1] 0.2371046

##

## $value

## [1] -0.6861689

##

## $counts

## function gradient

## NA NA

##

## $convergence

## [1] 0

##

## $message

## NULL